.svg)

Planning for retirement isn’t just about how much you save—it’s also about when you withdraw. One of the biggest and least understood risks retirees face is something called "sequence of returns risk."

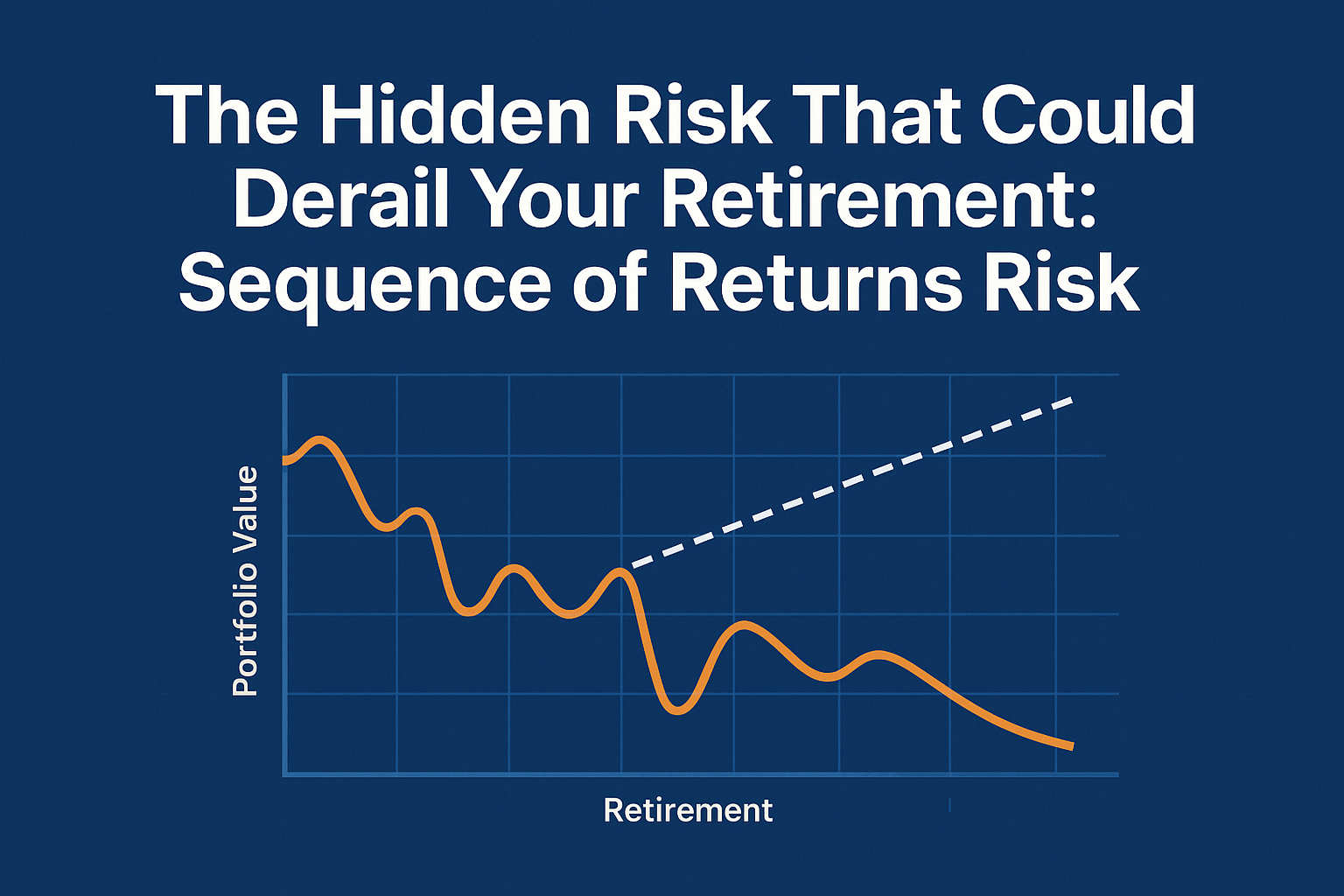

What Is Sequence of Returns Risk?

When you’re building your nest egg, the stock market’s ups and downs tend to average out over time. But once you start withdrawing money in retirement, the order (or sequence) of investment returns matters a lot more.

If you experience negative returns in retirement, while also withdrawing income, your portfolio may shrink faster than expected, and it may not have time to recover. That’s sequence of returns risk in action.

Why the Timing of Returns Matters

Let’s consider a simplified example:

- Retiree A and Retiree B both retire with $1 million.

- They both withdraw $50,000 per year.

- They both earn the same average annual return of 7% over 30 years.

- The only difference? Retiree A experiences a market downturn in the early years.

Despite the same average return, Retiree A may run out of money 10+ years sooner due to early losses plus withdrawals compounding the damage.

How This Risk Can Sneak Up on You

Sequence risk is unique to the retirement phase because:

- You’re withdrawing funds instead of contributing.

- Losses early on mean you’re “locking in” those losses.

- Your portfolio has less time to recover if the market rebounds later.

Even a modest bear market in the first few years of retirement can have a lasting negative impact—especially if you don’t have a strategy in place.

How to Protect Your Retirement Income

The good news is: you can plan around this risk. Here are a few strategies to consider:

1. Bucket Strategy

Break your assets into different “buckets” based on time horizon:

- Short-term (0–2 years): cash or cash equivalents for immediate needs

- Mid-term (3–7 years): conservative investments like bonds

- Long-term (8+ years): growth-oriented investments like stocks

This helps you avoid selling long-term investments at a loss when markets are down.

2. Flexible Withdrawal Strategies

Instead of withdrawing a flat dollar amount each year, consider:

- Withdrawing less in down markets

- Adjusting withdrawals based on portfolio performance

- Using dynamic withdrawal rules like the Guyton-Klinger or guardrails approach

This can help preserve your principal over the long term.

3. Guaranteed Income Sources

Having some income that’s not tied to market performance reduces pressure on your portfolio. This can include:

- Social Security

- Pensions

These can provide a reliable income floor, especially during volatile years.

4. Delay Social Security

Delaying benefits until age 70 can increase your monthly check significantly. This:

- Provides more guaranteed income

- Reduces the need to withdraw from your portfolio early on

- Acts as a hedge against longevity and market risk

5. Use Roth Accounts Strategically

Withdrawals from Roth IRAs are tax-free and don’t count toward your taxable income. In down years, pulling from a Roth account instead of traditional assets may reduce the impact of sequence risk and manage your tax brackets more effectively.

The Importance of a Personalized Retirement Plan

Every retiree’s situation is unique. A well-constructed retirement income plan takes into account:

- Your expected lifestyle expenses

- Market volatility

- Tax considerations

- Health care costs

- Legacy goals

Sequence of returns risk is just one piece of the puzzle, but it’s a critical one that’s often overlooked by DIY investors.

Work With a Financial Advisor Who Understands the Risks

Planning for retirement isn’t just about picking investments. It’s about crafting a strategy that gives you peace of mind—no matter what the market does.

A good financial advisor will:

- Stress-test your retirement plan against poor market timing

- Create a diversified income strategy tailored to your needs

- Help you stay on course, even in turbulent markets

Don’t Let Bad Timing Derail a Great Retirement

You’ve worked hard to build your nest egg. Make sure your withdrawal strategy protects it.

Schedule a free discovery call to learn how we help clients retire with confidence even when the market throws a curveball.

Disclosures:

Provided content is for overview and informational purposes only and is not intended and should not be relied upon as individualized tax, legal, fiduciary, or investment advice. Investing involves risk which includes potential loss of principal. Past performance is not a guarantee of future results. The use of asset allocation or diversification does not assure a profit or guarantee against a loss. Upon clicking third-party external links, you will access content that is not controlled, reviewed or approved by, and is not the responsibility of, the entities and individuals who provided the content you are leaving.